By Nathan P. Novak, Managing Director, Chicago

In the valuation of an operating business, the financial projections applied in the analysis can have a significant effect on the overall value conclusion. In many cases, the valuation professional (the “Analyst”) is provided financial projections that were prepared by the management team of the subject business. By performing due diligence, an Analyst can become comfortable that such financial projections are reasonable and representative of the expected future cash flow of the business—and, thus, reliable for use within an analysis.

Introduction

Financial projections are often an important input during the valuation process of an income-producing operating business. Many valuation methods incorporate a financial look ahead in some way, so as part of the valuation process, the Analyst is tasked with identifying the appropriate projections to rely on for the subject business.

During a business appraisal, the Analyst typically will request any financial projections prepared by the subject company management that are contemporaneous to the valuation date. It is often thought that such financial projections are the best source of cash flow expectations for a subject business. The management team lives and breathes the company operations every day, so who better to understand the performance nuances and expectations of the business? However, financial projections are often subject to significant scrutiny, particularly if a valuation analysis becomes contentious or is subject to a dispute.

Recent court cases shine a light on the importance of performing due diligence on management projections. In Pierce v. Commissioner, multiple sets of projections were prepared and relied on by various valuation experts. The issue of which set of projections to rely on (i.e., unadjusted management-prepared projections, adjusted management-prepared projections, or third-party advisor-prepared projections) became a key consideration in that case.1 Elsewhere, in Hyde Park Venture Partners Fund III v. FairXchange, LLC and In re PetSmart, Inc., management-prepared projections were criticized by the Delaware Court of Chancery (the “Chancery Court”) and ultimately found to be unreliable.2

Due to the importance and heightened scrutiny of management-prepared financial projections, there are several considerations and procedures that an Analyst may perform to become comfortable with management projections before relying on them within an analysis.

Analyzing the Preparation of Projections

Perhaps the first consideration an Analyst may make in deciding whether it is appropriate to rely directly on management-prepared projections is how and why those projections were prepared. The Chancery Court has often placed emphasis on management projections that were (1) prepared in the normal course of business, (2) prepared through a robust process (e.g., input from multiple managers throughout business units, approved by the board of directors, provided to third parties such as banks or advisors, etc.), and/or (3) not prepared for a specific, unique purpose, such as for use during litigation proceedings. Conversely, the Chancery Court has often rejected management projections when the opposite was true.3 That guidance from the Chancery Court is useful and sensible for an Analyst to consider during their own business valuation.

Upon the receipt of management-prepared projections, an Analyst may consider several relevant questions:

- When were the projections prepared?

- Why were the projections prepared (i.e., during the ordinary course of business or for some special purpose)?

- How often does management typically prepare projections throughout the course of the year?

- Does management ever update projections during the year?

- Who was involved in the preparation of the projections?

- What is the typical process for preparing projections (i.e., top down, bottom up, etc.)?

- What are the key assumptions that went into the projections, and is there support for each of those assumptions?

- In addition to the Analyst, who else have the projections been provided to (and why)?

- How are the projections used by the company?

There might be certain key individuals on the management team who “take ownership” of the projections. For example, that could be a senior person or group of people on the company finance team (e.g., the chief financial officer). Or, for a relatively small partnership, the controlling partner might be most informed on the projection process. Whatever the situation, it is often helpful for the Analyst to work with the key individuals on the management team who can provide insight into the projection process and answer those important questions.

The Analyst also may consider the sophistication of the subject business and, accordingly, the sophistication of the projection process. An Analyst might be more comfortable relying on projections that have been prepared using a robust and complex financial model, with direct input from the managers of all business units, compared to projections that have been prepared by one individual and are based only on a few broad assumptions. However, many smaller businesses do exactly that—they might not have a regular need for a detailed projection process or detailed projections. That alone does not indicate such projections are unreliable. It simply means that the Analyst may want to perform additional testing or added due diligence to become comfortable with the use of those projections within the analysis.

Evaluating Management’s Projections

Once the Analyst becomes comfortable that the process used to prepare the management projections was robust and objective, the question then becomes how accurate are the projections themselves? Even if management projections were prepared using a consistent, reliable process, it might be that the company tends to miss its projections each year (i.e., underperform or outperform), for one reason or another. To gain additional comfort and support for the use of management projections, the Analyst may assess management’s ability to accurately forecast the financial results of the business.

When requesting information during a business valuation, the Analyst might ask for (1) contemporaneous projections and (2) projections prepared in prior years or periods. Although older projections might not be relied on in the analysis, they can be helpful to assess the accuracy of management projections. For example, in addition to requesting five years of prior annual financial statements, the Analyst also might request five years of prior annual projections. The Analyst then may compare the prior projected results to actual results to gauge the accuracy of management’s projection process and whether any trends emerge.

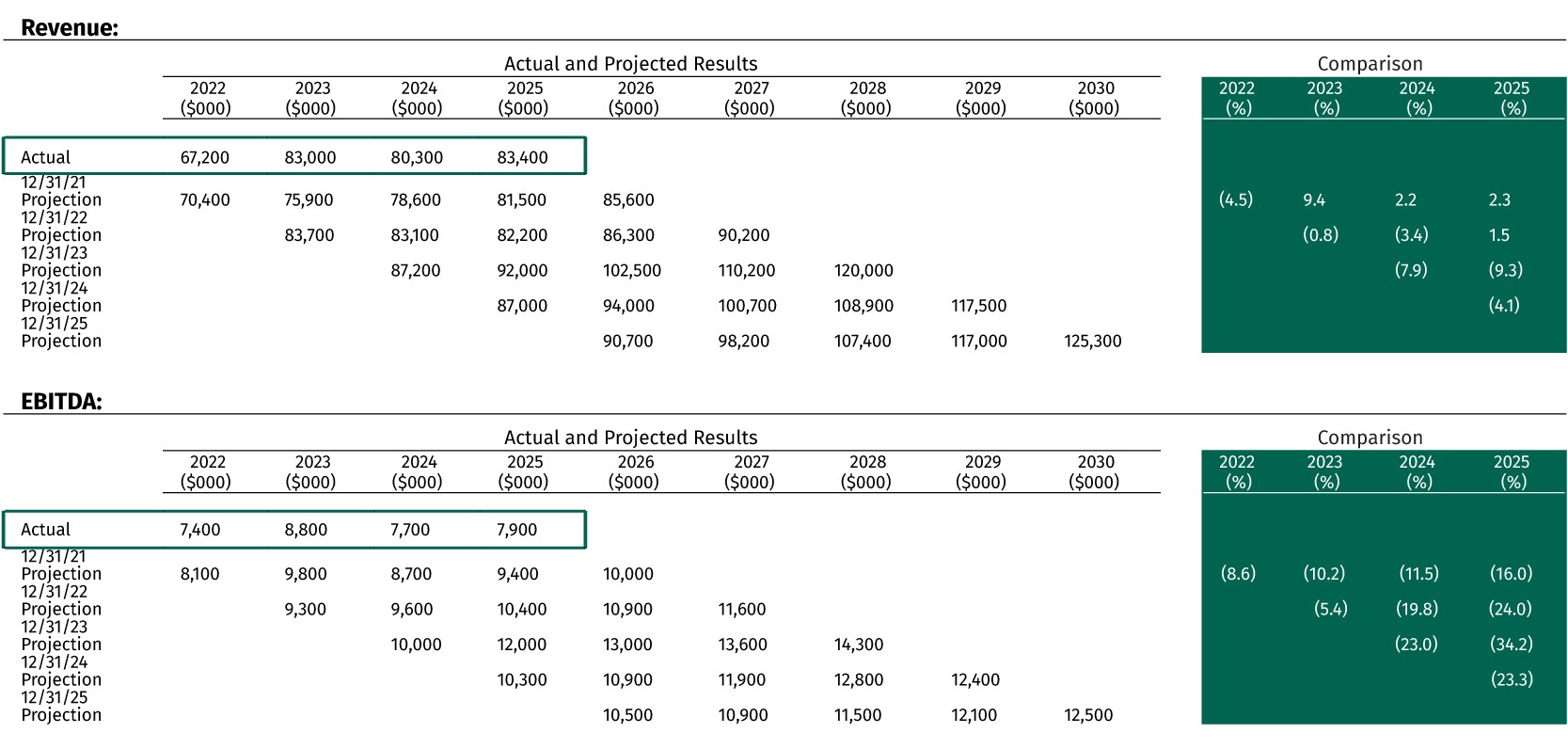

Table 1: XYZ Company Comparisons of Actual Versus Projected Performance

Table 1 presents an example of an analysis that may be used to assess management projections. In this example, the Analyst has been provided historical financial statements of the subject XYZ Company for fiscal 2022 through fiscal 2025, as well as annual projections that have been prepared each year for the past five years. The structure of the analysis is relatively simple—compare the projected results from prior sets of projections to the actual results.

As presented in Table 1, in this simplified example, the Analyst compared actual versus projected results for two metrics: revenue and earnings before interest, taxes, depreciation, and amortization (“EBITDA”). The boxes on the right side of the table indicate the percentage amount by which the actual results exceeded or failed to exceed the projected results each year.

The example analysis indicates that, generally, management projections for XYZ Company are relatively accurate from a revenue perspective. However, management is much less accurate with EBITDA projections, with the actual results differing from the projected results by double-digit percentages in most years. Further, it appears that XYZ Company management consistently over-projects the company’s EBITDA results (i.e., they consistently fall short of EBITDA targets).

The Analyst might use the above analysis to perform further due diligence regarding reliance on XYZ Company management projections. It might cause the Analyst to regroup with the management team to ask additional questions, such as whether there was a specific reason that they tend to miss EBITDA projections or whether they considered past EBITDA misses when preparing the current set of projections. It also might cause the Analyst to consider making certain adjustments to the projections or their application in the analysis, as described further below.

In addition to the metrics presented in the example above, an Analyst might compare any number of financial metrics to assess the accuracy of management’s projections, including other sensitive cash flow items, such as capital expenditures, working capital requirements, debt-free net income, and others. The Analyst might perform this comparison in dollar terms and other terms, such as margins or ratios.

In addition, the Analyst also might perform a similar analysis to any selected guideline publicly traded companies. For example, the Analyst might look at actual results of guideline public companies relative to historical projections to assess whether it is typical of other industry participants to miss or exceed targeted results. The goal is to perform those comparative analyses to identify whether certain trends or issues might be illustrated with respect to the management-prepared projections.

Adjusting for Management Projections

In many cases, after performing enough due diligence regarding the subject company management projections, the Analyst will conclude that those projections are a reliable indication of future expected cash flow and reasonable to apply within an analysis. However, in some instances, the Analyst might have concerns with the reliability of the management projections.

For instance, as indicated in the previous example, the Analyst might conclude that there are issues with the ability of management to accurately project future performance (e.g., management might be overly optimistic or pessimistic to the point that the projections might not be indicative of expected results).

However, it is often difficult (and might be inadvisable) for the Analyst to create an entirely new set of financial projections. After all, even if it is demonstrable that company management has a history of somewhat inaccurate projections, it still might be difficult to defend a de novo set of projections prepared by the Analyst who (1) might not be an expert on the specific industry in which the company operates, (2) might have begun working with the company and its management team only relatively recently, and (3) might not be knowledgeable about all the nuances of the company’s business.

In those instances in which the Analyst is uncertain as to whether the management projections are reliable, the analyst faces a decision—perform additional due diligence and work with the management team to become comfortable with the projections (and address the reasons why they might appear unreliable) or make certain adjustments to the analysis. If the Analyst decides that adjustments are necessary for a credible analysis, there are often two options.

The first option is to adjust the projections directly. For example, if the Analyst decides that management projections are consistently overoptimistic, the Analyst might make a downward adjustment to the projections to make them more in line with expected performance. That is, of course, the most direct option, and the Analyst should have explicit support as to (1) why it was appropriate to adjust the management projections and (2) the resulting projected figures.

The second option is to adjust other metrics in the analysis to reflect the heightened uncertainty regarding the management projections. Within a discounted cash flow method analysis, this could be factored into an adjustment to the present value discount rate. For example, the Analyst might conclude it is reasonable to make an upward adjustment to the discount rate to reflect overly optimistic management projections and, therefore, a higher risk of not achieving those projections. Or, in the context of a market approach, the Analyst might conclude it is reasonable to apply a pricing multiple toward the lower end of an indicated range to projected earnings or revenue to similarly reflect the projection risk.

Summary and Conclusion

Financial projections are often one of the most important inputs in the valuation of an operating business. Accordingly, it is important for an Analyst to perform proper due diligence regarding any projections provided or developed during the valuation analysis.

There are several steps that an Analyst may take to become comfortable with the reliability of management-prepared projections, including discussions with the management team and comparative analyses to identify any trends or biases with the typical projection process. In instances in which the Analyst concludes adjustments are reasonable, there are multiple ways to incorporate those adjustments that result in a credible analysis.

About the Author

Nathan P. Novak is a managing director of Willamette Management Associates and office director of the firm’s Chicago office. He can be reached at (773) 399-4325 or at npnovak@willamette.com.

References:

- Pierce v. Commissioner, T.C. Memo 2025-29 (April 7, 2025).

- See Hyde Park Ventures Partners Fund III v. FairXchange, LLC, Del. Ch. Memo (July 30, 2024); and In re Appraisal of PetSmart, Inc., Del. Ch. Memo (May 26, 2017).

- In re Appraisal of PetSmart, Inc., Del. Ch. Memo (May 26, 2017).